Your family knows about the house. They know about the car. But do they know about the $47,000 sitting in your Coinbase account? The Amazon storefront that brings in $3,000 every month? The life insurance policy you signed up for three years ago and never mentioned?

Modern wealth doesn't live in one place anymore. It's scattered across platforms, accounts, and jurisdictions that most families don't even know exist.

And when something happens - when life becomes uncertain, that wealth doesn't get transferred to the people you love. It just vanishes.

How wealth became invisible

Twenty years ago, you could count your wealth on one hand.

A bank account. A house. Maybe some stocks you bought through a broker. A car. That was it. Most people could list everything they owned in under five minutes.

Today, try the same exercise. Start with the obvious things - your checking account, your mortgage, your 401(k). Now keep going.

There's the crypto wallet you opened in 2020 when everyone was talking about Bitcoin. The Substack newsletter you started that now brings in a few hundred dollars a month. The Amazon FBA business you launched during lockdown. Stock options from your last company that vested but you haven't touched. Those domain names you bought on a whim that might actually be worth something. Your Roth IRA that auto-debits every month. The HSA you opened for tax benefits. Four thousand dollars in airline points you've been saving. That life insurance policy you clicked through online one night and honestly forgot about.

None of it is in one place.

Most of it doesn't have a paper trail. And you're not hiding any of it - you're just living your life, working, building things, moving money between platforms the way everyone does now.

There's never been a moment where you sat down and made a master list of everything. Why would there be?

But to your family, all of that is completely invisible. And when something happens, they won't know where to start looking.

Matthew Mellon had $500 million in crypto. His family spent three years trying to access it.

In 2018, Matthew Mellon died suddenly at 54. He was a banking heir, an early crypto investor, and by all accounts, a sophisticated guy when it came to money. His estate was estimated to include $500 million in cryptocurrency.

His family knew the crypto existed. They knew it was worth a fortune. They had lawyers, they had resources, they had every possible advantage in this situation. It still took them three years to access it.

Three years of legal battles. Three years of probate proceedings. Three years of watching Bitcoin swing from $6,000 to $60,000 and back down while they couldn't touch a single coin.

The estate was frozen while his family tried to prove ownership, locate wallets, recover seed phrases, and navigate a legal system that had absolutely no framework for dealing with digital bearer assets.

This was a sophisticated investor with significant wealth, and the system still completely failed his family.

If it can happen to someone like Matthew Mellon, what happens to everyone else?

The three ways inheritance breaks down

When someone dies or becomes incapacitated, families run into the same three problems every single time, and each one is worse than the last.

First, they don't know what exists.

An industry study found that roughly 28% of families have no idea where all of their loved one's assets are located during estate administration. There's no central registry, no master list that gets automatically generated when someone dies. If you don't know to look for something, you won't find it.

And most people have assets they've never told anyone about - not because they're trying to hide anything, but because the conversation never came up.

Second, even when they suspect something exists, they don't know where to look.

Which crypto exchange did he use? Which brokerage? Which email is the login tied to? Is that business registered under his personal name or some LLC he set up? Which bank? Which country?

One person might have accounts spread across Coinbase, Binance, MetaMask, a Ledger hardware wallet, and a paper wallet buried in a safe deposit box somewhere.

If they die tomorrow, how does anyone know which platforms to even start checking?

Third, even when they figure out what exists and where it is, they still can't get in.

Passwords are unknown. Two-factor authentication is tied to a phone that's been wiped or recycled. Platform terms of service explicitly prohibit account sharing, even when you show up with a death certificate. Companies demand court orders, and even when you get one, many of them still refuse.

Google has denied families access to deceased loved ones' accounts. Instagram has locked out surviving spouses. Coinbase has cited company policy to block legitimate heirs who showed up with every piece of legal documentation imaginable. The probate process in the United States takes 18 to 24 months on average, and during that entire time, crypto portfolios are swinging wildly, businesses are shutting down, subscription income is stopping, and value is eroding.

If you have assets across borders - property in one country, crypto in another, bank accounts in a third, the timeline stretches into years. You're dealing with multiple legal systems, multiple jurisdictions, and compounding delays at every step.

When someone is incapacitated but not dead

Here's something most people never think about until it happens to them: death isn't the only event that triggers all of this. Incapacitation can be just as catastrophic.

We've heard from people dealing with this firsthand.

In one case, a husband had a stroke and ended up in a vegetative state. His wife has been fighting through the court system for three years just trying to get access to their accounts - accounts they both assumed would simply work when they needed them. They don't. She's already dealing with the trauma of her husband being incapacitated, and now she's battling the legal system on top of it.

The system is designed for two states: fully alive and capable, or dead. There's no middle ground, and when you're stuck in that middle ground, everything breaks down.

Between 20% and 40% of all Bitcoin is gone forever

Chainalysis estimates that at least 20% of all Bitcoin that's ever been issued is permanently lost. Not hacked, not stolen, just lost. Because someone died and no one knew the seed phrase. Because a hard drive crashed and there was no backup. Because a piece of paper got thrown away during a move. Because the owner went into a coma and can't tell anyone where the wallet is.

Cryptocurrency is what's called a bearer asset, which means whoever physically holds the private key owns it outright.

There's no bank to call, no customer service department, no recovery mechanism. If you lose access to the key, the money is gone forever. This is by design, it's what makes crypto secure and decentralized in the first place. It's also what makes inheritance nearly impossible without an actual plan.

You can't just put your seed phrase in a will that goes through probate, because probate becomes public record. Anyone could look it up, see the seed phrase, and drain the wallet before your family ever gets access.

You can't give it to your lawyer either, because whoever has the seed phrase has complete control over the funds - they could disappear to the Cayman Islands the next day and there's nothing anyone could do about it.

You can't even store it in a regular password manager, because what happens if you're incapacitated and your family can't get into the password manager itself?

The security model that makes crypto work and the inheritance model that families need are fundamentally incompatible with each other.

Nobody's figured out how to solve that problem, until now.

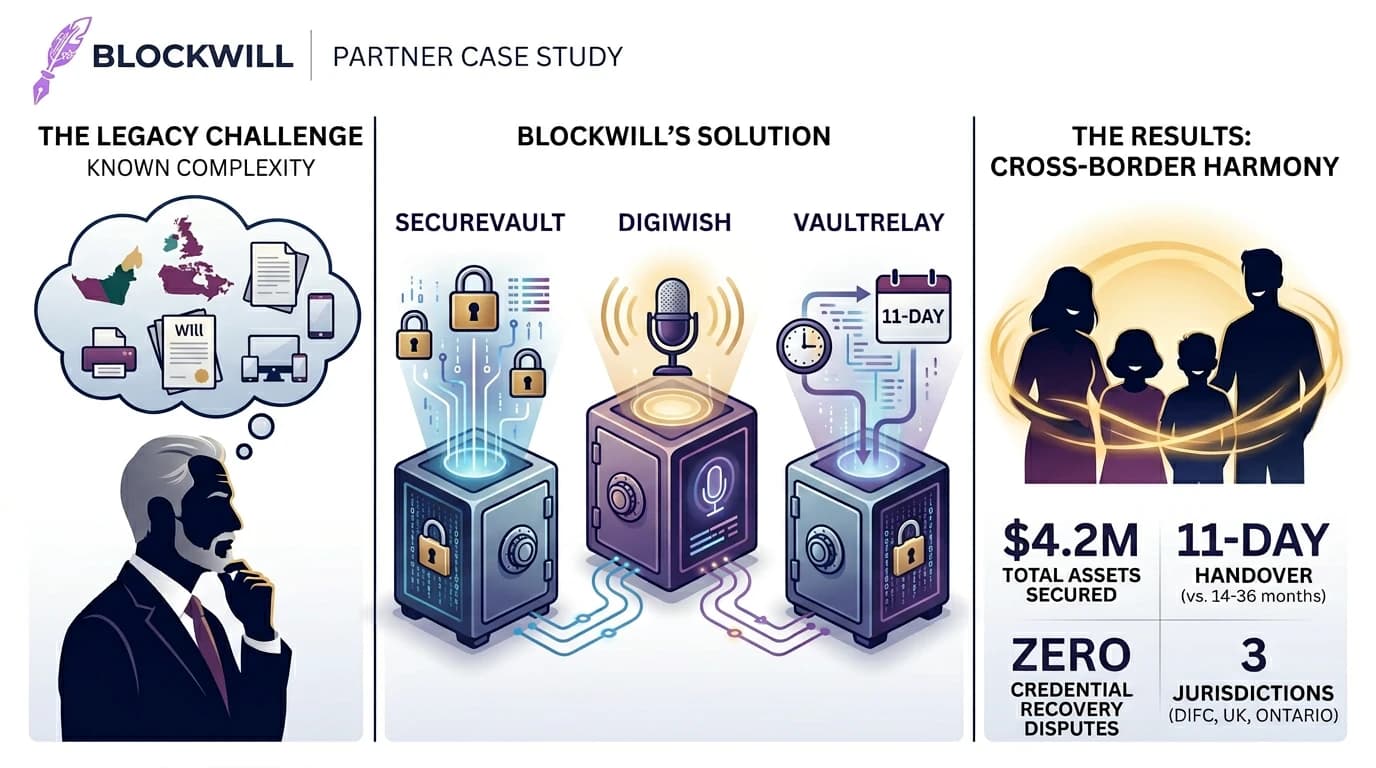

What BlockWill actually does

We built BlockWill to solve all three of those problems - existence, location, and access, in a single platform that works the way modern wealth actually works.

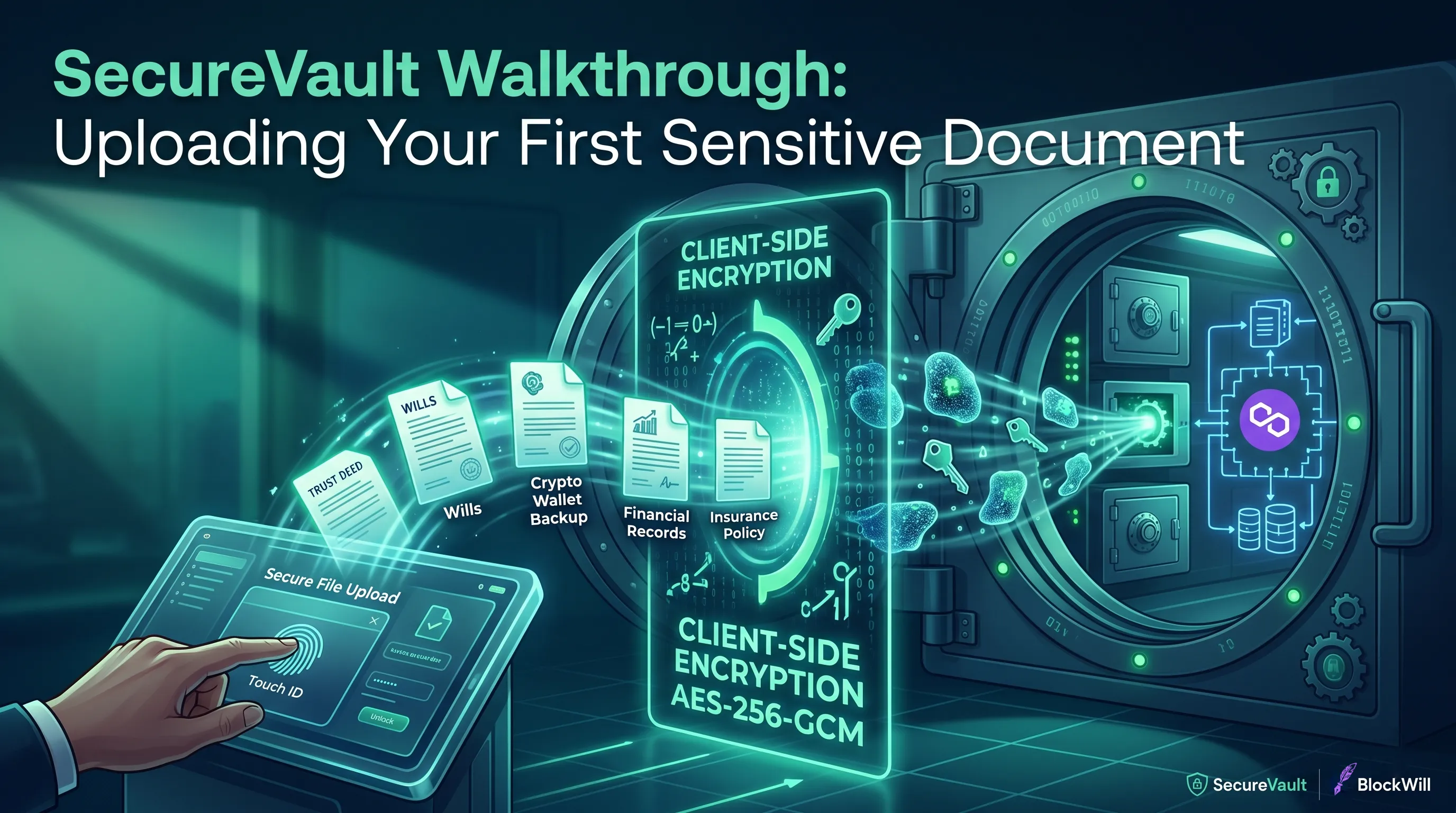

SecureVault is where you document every asset you own.

Not just the house and the car, but everything. The Coinbase account. The MetaMask wallet. The Amazon business. The life insurance policy you get through your employer. The domain portfolio. The startup equity. The investment accounts spread across three different countries.

For each asset, you don't just list it - you explain it. Where is it located? What's the login? What's the two-factor authentication method?

If it's crypto, where's the seed phrase stored, and how does someone who's never touched crypto in their life actually access it?

You leave instructions that are step-by-step and written in plain language, because the person inheriting your assets might not know what MetaMask is. They might not know how to import a seed phrase. They might not even know which email account is tied to which platform.

Everything you document is encrypted with zero-knowledge architecture, which means we can't read your data and neither can anyone else. It's protected with the same military-grade encryption used by intelligence agencies and secured with phishing-resistant hardware authentication that won't work even if someone clones our website letter-for-letter.

DigiWish is where you connect your assets to the people you want to have them.

This account goes to your wife. This one goes to your kids. This gets split three ways. This goes to your business partner when certain conditions are met.

It creates a single, verifiable source of truth about what you want to happen, and because every version of your wishes is hashed and timestamped on the blockchain, there's no confusion later. No conflicting wills from different years. No arguments about what you "really meant." Just an immutable record of your intent that courts are increasingly recognizing as legal proof.

VaultRelay is what actually gets the information to your family when they need it.

You set up three types of triggers: executor confirmation, inactivity detection, and time-based release.

If something happens to you, your designated executor can log in and activate the relay manually.

Within 24 to 48 hours, everyone you've designated gets instant access to all the information they need. If you don't log in for six months, the system starts sending you alerts, and if you still don't respond after the full period, it triggers automatically - even if your executor dies with you, your family still gets access. You can also set a specific date, like December 31, 2029, and the information will be released then no matter what happens. It's a final failsafe.

When any of these triggers activate, your family gets everything.

Every asset, every instruction, every piece of access information you've documented. Instantly, privately, and securely. No probate required. No lawyers arguing over what you meant. No family members spending months trying to reconstruct your financial life from old email receipts and bank statements.

What this actually means for you

BlockWill makes the invisible visible.

You get to see your entire financial life in one place, know exactly what you're worth, and know where everything actually is. More importantly, you know that if something happens - death, stroke, car accident, disappearance, your family won't spend years fighting through a system that was never designed for the way people live now.

Most people don't even realize what they own until they sit down and try to document it. Forgotten accounts. Small investments that have grown over the years. Subscriptions you're still paying for. Assets you didn't realize had any real value. Insurance policies you bought years ago and completely forgot about.

BlockWill gives you that complete picture, and it guarantees your family will get it too when they actually need it.