If someone asked you right now what your total net worth is, could you answer?

Not a rough estimate or "probably around something," but the actual number - every account, every asset, every investment, every piece of value you own, added up.

Most people can't. And it's not because they're careless or disorganized. It's because modern wealth doesn't live in one place anymore.

Where your money actually lives

Twenty years ago, calculating your net worth was straightforward.

You had a bank account, maybe a brokerage account, a house, a car. You could sit down with a pen and paper and have the number in fifteen minutes.

Today, try doing the same exercise.

Start with your checking account, then your savings, your 401(k), your Roth IRA, your HSA, your brokerage accounts - plural, because you probably have more than one. Add in stock options from current or former employers, any equity in private companies, real estate holdings, investment properties, the mortgage balance on each property, and home equity lines of credit.

Now add the things that didn't exist twenty years ago.

The crypto wallet you opened in 2020, maybe multiple wallets across different platforms. Ethereum staked somewhere. Bitcoin on an exchange. Maybe some altcoins you bought and honestly forgot about. NFTs that might have value or might be worthless, you're not even sure anymore.

There are online businesses too.

That Shopify store. The Amazon FBA business. The Substack newsletter with paid subscribers. The YouTube channel that's monetized. The online course you created that still generates passive income. Affiliate marketing arrangements. Domain names you bought that might be worth something.

Digital accounts have real value as well.

Airline points worth thousands of dollars. Hotel points. Credit card rewards. Unused gift cards. Refundable deposits with various services.

Then there are insurance policies - life insurance, disability insurance, long-term care insurance, that specialized policy you bought for one specific reason and haven't thought about since.

Business interests matter too.

Ownership stakes in LLCs. Partnerships in real estate ventures. Angel investments in startups. Crowdfunded equity positions. Fractional ownership in various assets.

If you've worked or lived abroad, you probably have assets held in different jurisdictions. That bank account you opened when you worked overseas. The investment account in another country. Property in a different jurisdiction. Foreign currency sitting in accounts you rarely check.

Physical assets with significant value add up as well. Jewelry, art, collectibles, watches, classic cars, equipment, tools, and inventory if you run a business.

Calculating your actual net worth now requires going through dozens of platforms, accounts, and assets spread across countries, currencies, and systems that don't talk to each other. And that's just what you remember.

What about the things you've forgotten? The account you opened five years ago and haven't logged into since, the automatic investment that's been running in the background, and the insurance policy you signed up for online and lost track of.

Why this actually matters

Not knowing your exact net worth affects the decisions you make.

Should you retire early? You can't answer that without knowing what you actually have.

Should you make a major purchase? That depends on your liquid assets, but do you know what those are across all your accounts?

Should you adjust your investment strategy? That's hard to do when you don't have a complete picture of your current allocation.

Beyond decision-making, there's the practical reality that if you don't know what you own, your family definitely doesn't know.

When something happens - when life becomes uncertain, they'll be starting from zero, trying to piece together what exists.

What knowing your worth actually requires

Knowing your worth means having a current, comprehensive view of everything you own.

For each asset, you need more than just "I have a Coinbase account." You need the account details, the login information, the two-factor authentication method, the recovery codes, instructions for how to access it, and notes about what's in it and why it matters.

For business interests, you need documentation of what you own, how it's structured, who else is involved, and how someone would verify ownership if they needed to.

For physical assets, you need records of purchase, proof of ownership, current estimated values, and location information.

For accounts in other countries, you need to document which institutions hold them, what the access process is, and any jurisdictional complexities someone would face.

This is about creating a complete financial map of your life that someone else - your spouse, your kids, your executor, your financial advisor could actually use.

How BlockWill approaches this

SecureVault is where you document every asset you own. Your crypto wallets, your online businesses, your investment accounts across three countries, your insurance policies, your stock options, your business ownership stakes, your physical assets with significant value, and the things you've built that generate value but exist only digitally.

For each asset, you document where it is, how to access it, what it's worth, and any context someone would need to understand it. This is for knowing what you actually have so you can make informed decisions and have a clear financial picture without spending two days trying to reconstruct it from scattered records.

If you work with asset managers or financial advisors, you can give them permission to document the assets they manage. They can help catalog everything with your oversight, but they can't move anything or access accounts. They have documentation permission without control.

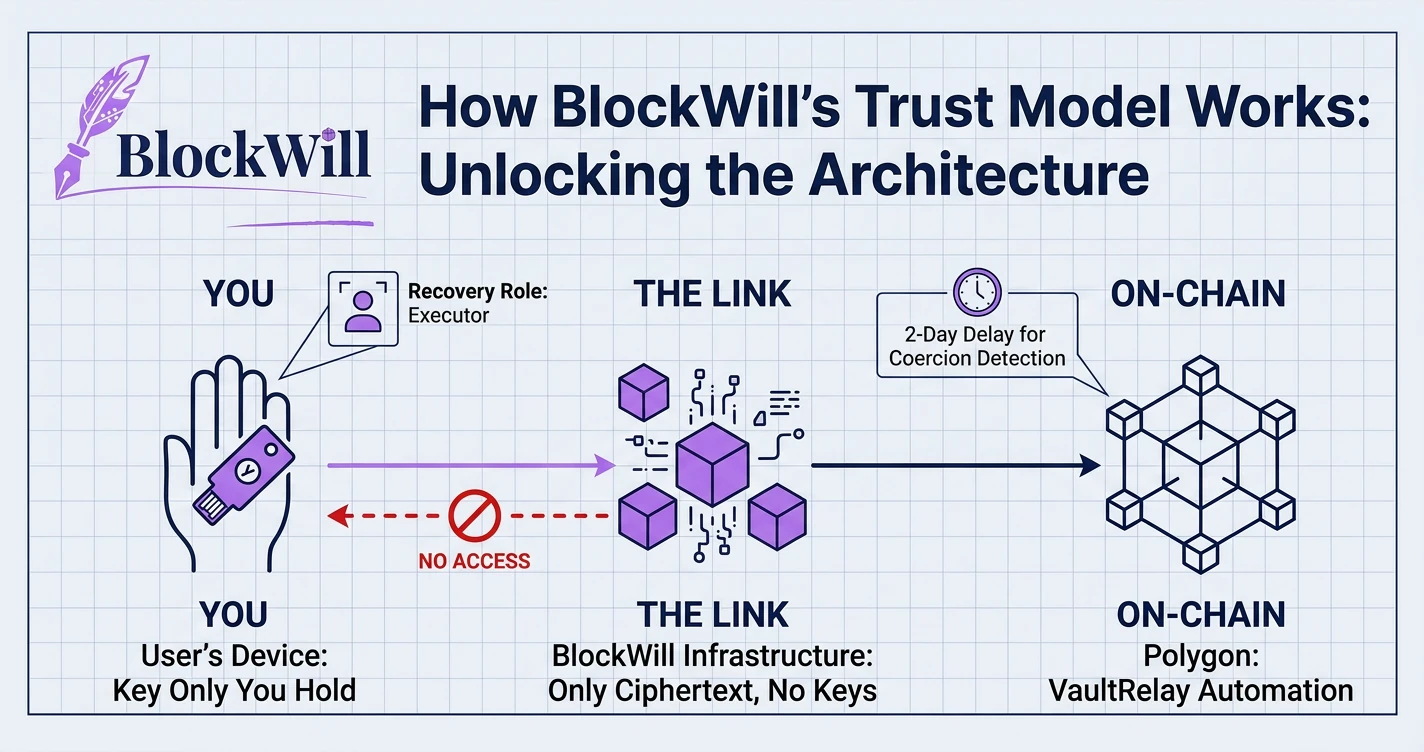

When something happens to you, your family gets instant access to everything through VaultRelay.

But even before that eventuality, they benefit from you finally knowing your actual worth because that knowledge affects how you manage your life right now.

What this looks like in practice

Let's say you're documenting your assets in SecureVault.

You start with your bank accounts - primary checking, savings, that high-yield savings account at a different bank you opened for better rates, the business account for your LLC. You note the institution, account numbers, login methods, and current balances.

You move to investments - your 401(k) through work, your Roth IRA at Vanguard, your brokerage account at Fidelity, another brokerage account you opened years ago at Schwab that you rarely check. You document each one with access information and current values.

You document crypto holdings. Your Coinbase account with Bitcoin and Ethereum, your MetaMask wallet with various tokens, that hardware wallet where you stored some crypto for long-term holding. You note where the seed phrases are stored and include step-by-step instructions for accessing each one, written for someone who's never used crypto before.

You document business interests - the LLC you own 60% of, the partnership in a real estate venture, the equity you got from an early-stage startup you advised, the Amazon FBA business generating a few thousand a month. For each one, you note the legal structure, your ownership percentage, how to verify it, and how someone would access or manage it.

You document real estate - your primary residence with the current mortgage balance, the rental property with mortgage and management company details, that piece of land you bought as an investment. For each property, you note where deeds are stored, what the current obligations are, and how someone would manage or sell it if needed.

You document insurance policies - life insurance through work and the private policy you bought, disability insurance, the umbrella policy. For each one, you note the carrier, policy number, beneficiaries, and how to file a claim.

You document other assets - the significant jewelry with appraisal documents, the collectibles that have appreciated, the equipment from your business, the domain names you own that might have resale value.

As you document each piece, you're building a complete inventory.

You can see everything in one place instead of having it scattered across platforms and filing cabinets. You realize you're worth more than you thought because you forgot about several accounts. You also realize you have more complexity than you'd acknowledged, and your family would have had no idea where to start.

Why do people avoid doing this

Most people don't create this comprehensive inventory because it feels overwhelming.

Where do you even start? How do you organize it? What level of detail matters? What if you forget something? What if it takes forever?

BlockWill removes those barriers by letting you start anywhere.

You add one asset, then another. You decide how much detail to include based on what would be useful. If you forget something, you add it later. You're building it gradually as you think of things rather than trying to complete everything at once.

What changes when you actually know

When you have a complete financial picture, decisions get clearer.

You can see if you're overexposed to certain assets. You can identify accounts you're no longer using that should be consolidated. You can spot opportunities you've been missing because you forgot certain assets existed.

You can have better conversations with advisors because you're working from complete information. You can set more accurate goals because you know your actual starting point. You can plan for the future with confidence instead of working with rough estimates.

When something happens to you, your family doesn't spend months trying to figure out what you owned. They get access to what you documented. They have the complete map you created and they can make informed decisions instead of guessing about what exists and where to find it.

Knowing your worth is all about clarity, and clarity is what makes everything else possible.