Al Mikial × BlockWill · Digital Assets Succession in the GCC

Rethinking Inheritance in the GCC: A Legal and Technological Framework for the Next Decade. A joint academic publication by Al Mikial Law Firm and BlockWill Analytical Technologies Limited.

1. Introduction: The Quiet Crisis in Digital Wealth Transfer

The twenty-first century will be defined, among other things, by the single largest intergenerational transfer of wealth in human history. Estimates place the global figure at well over USD 84 trillion by 2045, with the Gulf Cooperation Council (GCC) region alone accounting for approximately USD 1 trillion by 2030. A material and rapidly expanding share of that wealth does not sit in bank vaults, land registries, or share certificates. It sits on distributed ledgers, in encrypted wallets, across stablecoin balances, non-fungible tokens (NFTs), tokenised securities, cloud storage accounts, and protocol governance rights.

In the United Arab Emirates alone, licensed and unlicensed retail participation in virtual assets is estimated between twenty-five and thirty per cent of adults, with on-chain inflows exceeding USD 34 billion in recent measurement cycles. The asset class is no longer marginal; the legal architecture around its succession is.

This paper examines the widening gap between digital asset ownership and the legal frameworks that govern inheritance within the GCC, with particular focus on the Kingdom of Saudi Arabia (KSA) and the United Arab Emirates (UAE). Drawing on contemporary legal scholarship, newly promulgated statutes, and the evolving commentary of regional practitioners including the published analyses of Saudi-qualified counsel on blockchain, Sharia, and regulatory convergence, it argues that the protection of digital legacies in the region requires a deliberate convergence of doctrinal legal craftsmanship and cryptographically verifiable infrastructure. Neither discipline, acting alone, is adequate to the task.

2. The Scale of the Problem

Digital assets are unique among classes of property in a single, decisive respect: the loss of access is frequently indistinguishable from the loss of ownership. A forgotten seed phrase, an undisclosed hardware wallet, a lapsed two-factor authentication device - any of these can render an asset permanently inaccessible even where legal title is perfectly secure.

Empirical estimates suggest that between USD 75 billion and USD 140 billion of Bitcoin alone is believed to be permanently lost, much of it following the death or incapacity of the original holder. Where classical inheritance law presumes that the estate's components can be located, identified, and authenticated by an executor, digital estates invert the presumption. The asset exists; the heir cannot reach it.

The GCC is particularly exposed. The region combines very high retail and institutional crypto adoption with a multi-layered legal environment in which federal, emirate, free-zone, and Shariah jurisdictions each apply to different facets of a single estate. A Saudi national holding Ether in a self-custodied wallet, an apartment in Business Bay held by a DIFC foundation, and a life-insurance policy in London is, in legal terms, the custodian of three mutually incompatible succession procedures. The technology she uses to hold the Ether is global; the law that will pass it to her children is not.

3. The Regulatory Mood: A Saudi Practitioner's Perspective

Among the clearest contemporary commentaries on the region's regulatory trajectory is a sequence of analyses published in late 2023 and early 2024 by a California-qualified attorney practising in Riyadh. Writing in October 2023, she observed that the Saudi Central Bank (SAMA) had moved from a posture of warning to one of active infrastructure building, piloting distributed ledger technology for interbank settlement while preparing the ground for a central bank digital currency.

By January 2024, her analysis sharpened. Saudi Arabia's Crypto Embrace: From Warnings to Sharia Compliance charted the Kingdom's shift from prohibition-adjacent caution toward a framework in which virtual assets could be rendered Sharia-compatible through careful structuring and scholarly endorsement. Her concurrent work on digital twins - observing that the purchaser of an NFT "only owns a unique hash on the blockchain" - is a useful reminder that tokenised ownership in the GCC will live or die on the evidentiary weight courts attach to cryptographic artefacts.

These are not merely descriptive writings. They capture a practitioner's intuition that is essential to any honest appraisal of GCC digital inheritance: the regulatory direction of travel is settled, but the doctrinal tools - particularly for succession - have not yet caught up with the instruments they are meant to govern. Regulation is arriving upstream, at the point of issuance, custody, and transfer. Inheritance sits downstream, where the regulatory light is dimmer and the stakes, measured in grief as much as in riyals or dirhams, are highest.

4. The UAE's Fragmented Succession Architecture

4.1 DIFC: Common-Law Certainty with Narrow Aperture

The Dubai International Financial Centre (DIFC) has moved further and faster than any other jurisdiction in the region on the legal characterisation of digital assets. DIFC Law No. 2 of 2024 expressly classifies digital assets as a distinct third category of personal property, resolving the conceptual impasse that English common law itself only addressed through the UK Property (Digital Assets etc.) Act 2025. The DIFC Wills Service Centre pioneered a dedicated Digital Assets Will instrument, and DIFC Law No. 2 of 2025 broadened jurisdictional eligibility for non-Muslim testators.

These are substantial achievements. They are also narrow. The Digital Assets Will, in its current form, supports a closed list of six tokens - BTC, ETH, MATIC, USDC, USDT and HBAR - and does not accommodate NFTs, decentralised finance positions, liquidity-pool receipts, tokenised real-world assets, or on-chain governance rights. The instrument is, moreover, available principally to non-Muslim expatriates.

For Muslim residents of the UAE, mandatory Faraid shares under classical Islamic inheritance doctrine continue to govern, with testamentary freedom limited to the one-third Wasiya bequest. Parallel architectures such as emirate-level Shariah courts, federal personal-status law, and the ADGM's common-law counterpart, produce a landscape in which the choice of forum can materially alter the distribution of identical on-chain assets.

4.2 Federal Innovation: Waqf, Virtual Assets, and Evidence

At the federal level, three instruments are especially consequential for digital succession.

First, UAE Federal Decree-Law No. 51 of 2024 permits the conversion of private wealth, including financial instruments, into a waqf, the classical Islamic endowment, under modernised rules that contemplate contemporary asset types.

Second, CBUAE Federal Decree-Law No. 6 of 2025 imposes a September 2026 deadline for virtual asset service providers to be fully licensed, with attendant custody, reporting, and beneficiary-designation obligations.

Third, and most underappreciated, UAE Federal Law No. 35 of 2022 on Evidence expressly recognises electronic evidence, including documents whose integrity is guaranteed by cryptographic means.

Read together, these statutes provide the doctrinal scaffolding for a Shariah-compliant, federally enforceable, and cryptographically verifiable succession practice. The scaffolding exists; the instruments that would use it at scale do not yet.

5. Saudi Arabia: Sharia Sovereignty and the Evidentiary Frontier

The Saudi framework begins from a different premise. Under the Basic Law of Governance, the Qur'an and Sunnah are the constitution of the Kingdom, and inheritance is governed by the mandatory Faraid shares together with the one-third Wasiya allowance. There is no freestanding expatriate will registry analogous to DIFC's, and cross-border estate planning for resident non-Muslims has historically relied on home-country instruments of uncertain local effect.

The 2022 Saudi Law of Evidence introduced materially modernised treatment of electronic and cryptographic evidence, and the Personal Data Protection Law (PDPL), fully in force since 2023, imposes data residency and cross-border transfer requirements with direct implications for custodial key management.

Two currents are worth naming. The first is SAMA's steady, deliberate embrace of distributed ledger infrastructure, piloted in interbank settlement and preparatory CBDC work, which establishes a domestic technical base and, crucially, a regulator fluent in the primitives. The second is a visible openness in Saudi scholarship to Shariah-compliant tokenisation such as sukuk issuance on permissioned chains, fractionalised real-estate vehicles and Zakat-aware stablecoin models, that implies a willingness to contemplate digital instruments within the inheritance chain, provided their economic substance satisfies classical doctrinal tests. The practitioner commentary cited above captures this mood precisely: the regulatory posture is not one of rejection but of structured assimilation.

The succession gap in Saudi Arabia is therefore not primarily doctrinal. Faraid, properly applied to a correctly inventoried estate, is fully capable of handling digital property, but operational and evidentiary. Who holds the keys? How is the wallet's existence proven? How is a private key surrendered to a legitimate heir without violating PDPL, without compromising custody standards, and without contaminating the chain of evidence that a Saudi court would require?

6. The Evidentiary Problem at the Heart of Digital Succession

Seen in this light, the legal gap across the GCC is less a gap in substantive inheritance law than a gap in the evidentiary and executional infrastructure that any inheritance regime, Sharia or otherwise, requires in order to operate on digital property. Four interlocking problems recur in every jurisdiction surveyed.

First, asset discovery. Executors in Riyadh, Abu Dhabi, and Dubai routinely report that they cannot determine whether the deceased held any cryptoassets at all, let alone where.

Second, intent authentication. WhatsApp screenshots of private keys, printed seed phrases in a safe deposit box, and hand-written instructions attached to a will all fail the most basic tests of a court examining whether the decedent genuinely intended a particular transfer.

Third, conditional execution. Classical inheritance presumes a moment of unconditional transfer; sophisticated estate planning often requires conditional transfer on the completion of the Iddah period, on the attainment of majority by a ward or on the discharge of debts under Faraid priority rules, that paper instruments execute poorly and distributed ledgers execute natively.

Fourth, cross-border verifiability. A private key is meaningful in Singapore, in Riyadh, and in Dubai simultaneously; a certified copy of a will is not. Any serious regional framework must therefore be multi-jurisdictional by construction.

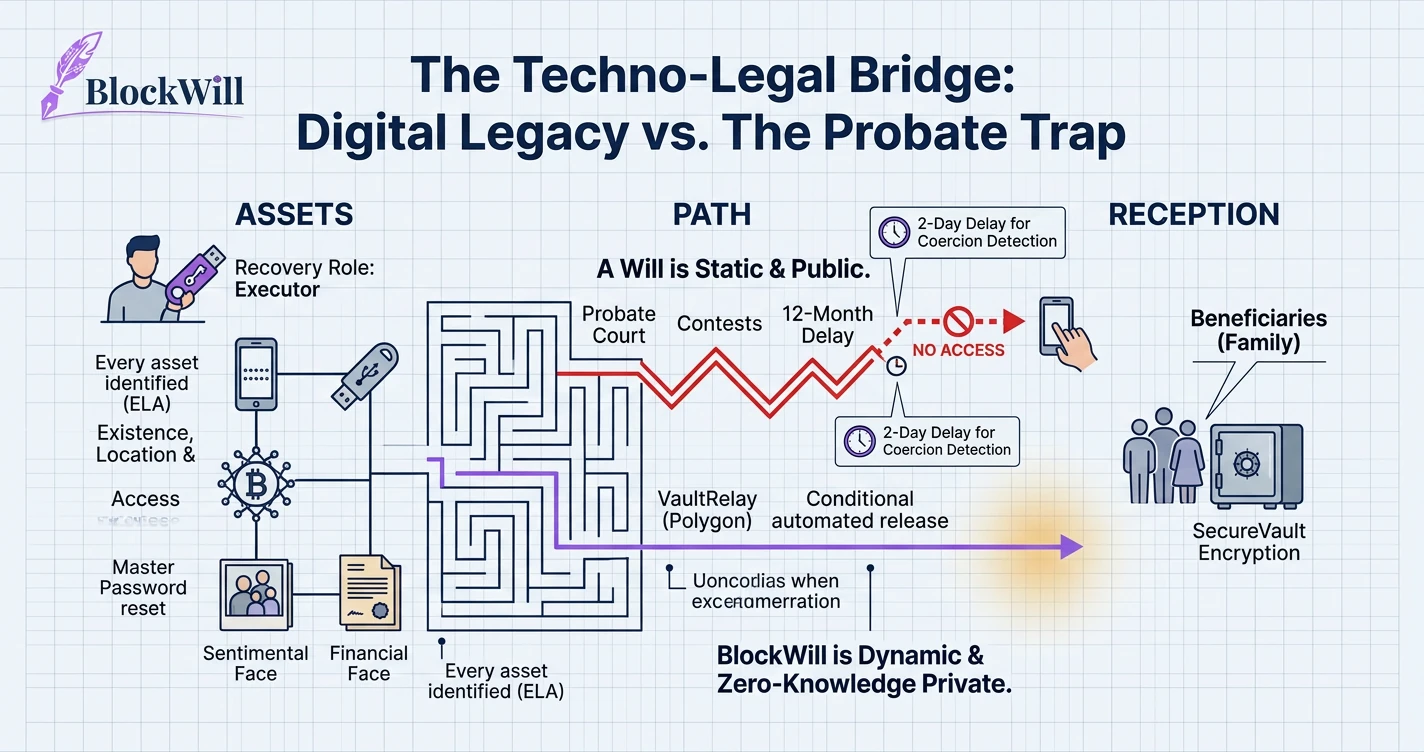

7. Blockchain Infrastructure as Succession Infrastructure

Blockchain technology, properly characterised, is not a competitor to legal process; it is a substrate for it. Three capabilities are particularly salient for succession practice in the GCC.

A cryptographic intent layer allows a testator's expression of wishes to be hashed at the moment of expression, timestamped, and anchored to a public chain. The hash does not disclose the content; it fixes it. Where a UAE or Saudi court is asked, years later, whether a given document represents the decedent's genuine instruction, the chain provides an evidentiary anchor more robust than the witness-based testimonies on which classical testamentary law has relied for centuries. This is squarely contemplated by Article 17 onward of UAE Federal Law No. 35 of 2022. It is not displaced by Saudi Arabia's 2022 Law of Evidence; it is precisely the kind of technical artefact that the 2022 Law contemplates.

A zero-knowledge custody layer - where encrypted key material is held under multi-party computation, with access conditioned on judicially cognisable triggers - resolves the tension between PDPL-style data-residency rules and the realities of global wallet custody. The custodian holds nothing in the clear; the heir receives access only upon a condition whose occurrence is itself verifiable on-chain. This architecture is neither speculative nor experimental; it is the operating pattern of leading institutional custodians, and it is wholly consistent with the principles expressed in contemporary legal scholarship on the governance of digital property.

A programmable delivery layer, sometimes known as a dead-man's switch, converts the conditional transfers that estate planners have always drafted on paper into executable instructions. Faraid priorities, Wasiya caps, Iddah periods, waqf conditions, guardianship milestones - each is expressible as a state transition whose trigger is a verifiable fact: a death certificate hash, a court order, a DIFC probate grant or a reaching of age. The programmable layer does not decide the legal question; it executes the legal answer.

8. The Way Forward: Doctrinal Depth Meets Programmable Infrastructure

The emerging international consensus - from the UK Law Commission's 2023 report and the resulting Property (Digital Assets etc.) Act 2025, through the European Union's Markets in Crypto-Assets Regulation, to DIFC's Digital Assets Law No. 2 of 2024 - is that digital property is property. That settles the jurisprudential starting point. It leaves open the operational question that the GCC must now answer: how is such property inherited, safely and faithfully, under the region's plural legal traditions?

The honest answer involves two disciplines working in concert. The first is a regional legal practice capable of drafting instruments that operate in Arabic and English, in Shariah and common-law registers, and across emirate, federal, and free-zone jurisdictions simultaneously - a practice that specialist regional firms have begun to build, often in collaboration with Saudi-qualified and DIFC-registered counsel. The second is technical infrastructure built to the standards of institutional financial services: zero-knowledge custody, cryptographic timestamping, oracle-verified conditional execution, and auditable compliance with PDPL, the DIFC Data Protection Law, and CBUAE Decree-Law No. 6 of 2025.

Neither discipline, alone, succeeds. A beautifully drafted DIFC Digital Assets Will is of limited use if the executor cannot locate the wallets it purports to bequeath. Equally, a cryptographically flawless delivery protocol that contravenes Faraid shares or violates PDPL data residency requirements is worse than useless: it is a compliance liability that will not survive a Saudi or ADGM court's first scrutiny. The frontier of digital succession practice in the GCC is therefore a frontier of collaboration - between counsel who understand the doctrinal terrain and technologists who understand the evidentiary primitives.

The stakes are not abstract. Only eighteen per cent of GCC family businesses report a formalised succession plan; approximately one-third of Middle East family offices require explicit Shariah compliance in any inheritance instrument they adopt. These are populations for whom legacy is not a portfolio decision but an ethical and religious obligation. The mismatch between that obligation and the present state of digital-asset infrastructure is the single most consequential private-client question the region will confront in the coming decade.

9. Conclusion

Blockchain technology did not create the problem of digital succession; it merely made it impossible to ignore. The asset class has grown faster than the doctrinal tools designed to transmit it, and the GCC, by virtue of its wealth, its demographic velocity, and its distinctive plural legal order, sits at the leading edge of the mismatch.

The region is, however, equally well positioned to lead the response. Its free zones have produced some of the most advanced common-law treatment of digital assets anywhere in the world. Its federal instruments - on waqf, on evidence, on virtual asset regulation - are compatible with, and in places anticipatory of, international best practice. Its Shariah tradition, properly read, is not hostile to programmable instruments; it is, in fact, natively at ease with conditional transfers, fiduciary structures, and the public verification of private commitments.

What the region now requires is the patient, deliberate construction of succession instruments that meet both the doctrinal demands of its courts and the evidentiary demands of the chains on which its wealth increasingly sits. This is the shared work of lawyers and technologists, an opportunity for practitioners who can interpret a Saudi fatwa on tokenised securities and engineers who can build the cryptographic rails that make the fatwa executable. Initiatives that bring these competences together - whether through bar-led working groups, regulator-led sandboxes, or private collaborations between regional counsel and legal-tech infrastructure providers - are the most credible path to an inheritance framework that honours the region's legal heritage while embracing the assets its next generation will actually own.

The wealth is already on-chain. The question is whether the law can meet it there. The answer, across Riyadh, Abu Dhabi, and Dubai alike, will be written by those willing to do the unglamorous yet honourable work of closing the gap.

References

[1] Awni, Jeanina. Is Saudi Arabia ever going to approve blockchain regulations? LinkedIn Article, 17 October 2023.

[2] Awni, Jeanina. Saudi Arabia's Crypto Embrace: From Warnings to Sharia Compliance - A Shift in Perspective. LinkedIn Article, January 2024.

[3] Awni, Jeanina. Digital Twins: Legal Considerations for an Emerging Technology. LinkedIn Article, 6 December 2023.

[4] Awni, Jeanina. Crypto, Securities, and Sharia: A Comparative Analysis of U.S. and Saudi Legal Approaches. LinkedIn Article, 2023-24.

[5] Boston Consulting Group. Global Wealth Report: The Tipping Point. Boston: BCG, 2023.

[6] Cambridge Centre for Alternative Finance. 3rd Global Cryptoasset Benchmarking Study. Cambridge: CCAF, 2022.

[7] Campbell-Verduyn, Malcolm, and Moritz Hütten. The Formal, Financial and Fraught Route to Global Digital Asset Governance. New Political Economy 24, no. 6 (2019): 821-842.

[8] Central Bank of the United Arab Emirates (CBUAE). Federal Decree-Law No. 6 of 2025 on the Regulation of Virtual Asset Service Providers.

[9] Chainalysis. Middle East & North Africa Crypto Adoption Report 2024. New York: Chainalysis, 2024.

[10] De Filippi, Primavera, and Aaron Wright. Blockchain and the Law: The Rule of Code. Cambridge, MA: Harvard University Press, 2018.

[11] Dubai International Financial Centre. DIFC Law No. 2 of 2024 (Digital Assets Law).

[12] Dubai International Financial Centre. DIFC Law No. 2 of 2025 (amending the DIFC Wills and Probate Registry Rules).

[13] DIFC Wills Service Centre. Digital Assets Will: Product Note, 2023.

[14] Financial Action Task Force (FATF). Updated Guidance for a Risk-Based Approach to Virtual Assets and VASPs. Paris: FATF, 2021.

[15] Kingdom of Saudi Arabia. Basic Law of Governance. Royal Order No. A/90, 1992.

[16] Kingdom of Saudi Arabia. Law of Evidence. Royal Decree No. M/43 of 2022.

[17] Kingdom of Saudi Arabia. Personal Data Protection Law. Royal Decree No. M/19 of 2021, as amended 2023.

[18] Knight Frank. The Wealth Report 2024. London: Knight Frank, 2024.

[19] KPMG and Agreus. Global Family Office Compensation Benchmark - Middle East Edition. 2024.

[20] PwC Middle East. Family Business Survey - GCC Edition. Dubai: PwC, 2024.

[21] Saudi Central Bank (SAMA). Rules Governing Open Banking, 2022.

[22] UAE Federal Decree-Law No. 51 of 2024 concerning the Regulation of the Waqf Sector.

[23] UAE Federal Law No. 35 of 2022 on Evidence in Civil and Commercial Transactions.

[24] United Kingdom. Property (Digital Assets etc.) Act 2025.

[25] UK Law Commission. Digital Assets: Final Report. Law Com No. 412. London: HMSO, June 2023.