Why a will is no longer enough - and what the GCC's $1 trillion wealth transfer needs next.

By 2030, roughly one trillion US dollars will change hands across the families of the Middle East and North Africa. It will be the largest wealth transfer this region has ever seen. And by every credible measure, the families involved are not ready.

Only 24% of MENA HNIs have a comprehensive estate plan in place. Among GCC family businesses, the figure is even sharper - just 18% have a real succession plan. Behind those numbers sit thousands of widows, sons and daughters who, when the moment comes, will not know where to look. Not for the keys. Not for the documents. Not for the passwords, the wallets, the accounts, the property deeds, or the wishes of the person who has just left them.

I want to tell you about a man named Stefan Thomas. Somewhere in San Francisco, he stares at a USB drive worth roughly 777 million dollars that he cannot open. He has used eight of his ten password attempts. After two more, the drive will erase itself, and the fortune will sit on the blockchain forever - visible, untouchable, eternal.

I am telling you Stefan’s story not because he is unusual. I am telling you because, in a quieter way, almost every MENA family with digital wealth is one careless moment away from the same outcome.

The trillion-dollar problem nobody is solving

Let us be honest about the scale.

The GCC’s wealth has roughly tripled in two decades. UAE HNI wealth alone has surged about 20% since 2022, now sitting around 700 billion dollars. Dubai’s financial hub hosts family offices overseeing 1.2 trillion dollars. The UAE is projected to net nearly 9,800 millionaires in 2025 alone - the highest inflow of any country on earth.

And yet, the Lombard Odier 2025 GCC Succession Planning Survey found that 49% of HNW families without a plan continue to postpone the process. Nearly 60% of Saudi HNIs view succession as “a future concern.” A separate DIFC, Julius Baer and Euroclear study found that 73% of wealth holders in the region are unwilling to discuss legacy planning even with their most trusted advisors.

The result is what I call the silent leakage. More than half of all wealth transfers in the region face delays. Frozen accounts. Translation costs. Court filings. Family meetings that turn into arguments. Investment positions that drift while paperwork moves at the speed of bureaucracy.

This is not an inheritance problem. This is a coordination problem at civilizational scale. And the coordination is failing because the tools we have are tools designed for a world where wealth was paper - title deeds, share certificates, locker keys, bank passbooks. That world is gone.

The new shape of wealth - crypto, accounts, photos

Look at any modern MENA HNI’s balance sheet, and you will see how the shape of wealth has changed.

74% of family offices have invested in or are exploring crypto today, up 21 percentage points in 12 months according to BNY Wealth’s 2025 Single Family Office study. 86% of US family offices became more crypto-curious after the 2024 election. The MENA region - with VARA in Dubai, ADGM’s regulatory clarity and the DIFC Innovation Hub - is one of the fastest-moving jurisdictions in the world for institutional digital asset adoption.

But here is the uncomfortable truth: the same security model that protects your digital wealth from attackers also protects it from your own family.

Consider the four cases that should haunt every MENA wealth holder.

Stefan Thomas. The Silicon Valley programmer who received 7,002 BTC in 2011 for making a video about Bitcoin. He stored them on an IronKey USB drive and lost the password. The drive self-destructs after ten wrong attempts. He has used eight. “I would stay up all night trying different ideas,” he told one journalist, “or just staring at the ceiling for hours.” At 2025 prices, his locked fortune is worth around 777 million dollars.

James Howells. A Welsh engineer whose ex-partner, in 2013, accidentally took his hard drive containing 8,000 Bitcoin to the Newport landfill. After twelve years of legal battles, the UK High Court dismissed his case in January 2025. The drive is buried under 25,000 cubic metres of waste - close to a billion dollars of permanently inaccessible Bitcoin sitting under the Welsh earth.

Gerald Cotten. The 30-year-old founder of QuadrigaCX, Canada’s largest crypto exchange. Died suddenly in India in December 2018 - twelve days after signing a will that left a 100,000-dollar trust to his two chihuahuas, but no plan for the cold-wallet passwords for 115,000 customer accounts. Approximately 190 million dollars of customer assets froze on the blockchain that day.

The North Carolina widow. Less famous, more important. After her husband’s death, she discovered he held over 200,000 dollars in cryptocurrency. He never told her where the wallet was. He never wrote down the seed phrase. Her will named her sole heir. The court could not access the funds. They still exist on the blockchain, untouchable.

Between 2.3 million and 3.7 million Bitcoin are estimated to be permanently lost - between 11% and 18% of the entire fixed supply, worth somewhere between 140 billion and 466 billion dollars at current prices. Most of these losses had nothing to do with hacks or scams. They were inheritance failures. They were people who died, or forgot, or lost a piece of paper.

The probate trap in MENA

If you live in the GCC, you face a layer of complexity most jurisdictions do not.

88% of UAE residents are expats. Most of them carry assets in two, three or four countries. Most of them are governed by overlapping legal systems - UAE federal law, Sharia personal status law, DIFC common law, ADGM common law, plus the law of their home country. Without a registered will in the UAE, Sharia inheritance rules apply by default, regardless of whether the deceased was Muslim. Sons receive twice the share of daughters. Spouses receive fixed minimums. Even distant relatives may have entitlements.

For non-Muslim expats, Dubai Law No. 2 of 2025 has been a meaningful step forward. It granted DIFC Courts exclusive probate jurisdiction over registered non-Muslim wills, including assets located outside the DIFC. DIFC-registered wills now flow through directly to the Dubai Land Department, the RTA and UAE banks - without the historic conversion step through Dubai Courts.

But “faster” is not “fast.” A clean DIFC probate still takes weeks. A contested or document-incomplete estate stretches into many months. And for assets held in the wider GCC, in India, in the UK, in Singapore - every additional jurisdiction is a new clock, in a different time zone, in a different language, in a different legal tradition.

In the meantime: bank accounts freeze immediately upon notification of death. Joint accounts freeze. Business signing authorities pause. Share registers cannot be updated. School fees come due. Rent comes due. Lawyers and translators come due. Currency moves. Markets move. Family conversations turn from grief to suspicion.

The estate value erodes in five quiet ways while heirs wait - legal and translation fees, frozen business operations, currency depreciation, lost investment opportunity, and the most expensive line item nobody puts in a spreadsheet - family conflict. 45% of GCC families cite difficulty reaching agreement as the top barrier to succession.

What “digital legacy” actually means

Most people, when they hear the phrase “digital legacy,” picture a will with a few crypto wallet addresses written in. That is not what we are talking about.

A digital legacy is the entire body of electronic information, accounts, assets and identity a person leaves behind. It has two faces.

The financial face includes crypto wallets, exchange accounts, online brokerage and demat accounts, mutual fund folios, dormant bank accounts in five countries, life and investment-linked insurance policies, NFTs, DeFi positions, IP and royalties, social media monetisation, frequent flyer miles, loyalty points, and - perhaps most critically - the master password to the email account that controls every other password reset in your life.

The sentimental face is photographs, videos, voice notes, journals, the family WhatsApp group, the last text messages, the iCloud library full of two decades of birthdays. In October 2023, an Ohio family discovered that 4,200 photographs of their late father were locked behind a single master password none of them knew. The financial loss was zero. The human loss was incalculable.

The numbers on the planning gap are sobering. Only 24% of internet users with a will mention any online account information in it. 34% have not shared digital assets with anyone at all. Only 30% of people in long-term relationships say their partner could easily access their online accounts after their death. The average person manages between 100 and 168 passwords. Apple’s Legacy Contact, Google’s Inactive Account Manager and Facebook’s Legacy Contact all exist - and almost no one uses them.

We obsess over preserving wealth. We rarely talk about preserving the things that make wealth worth preserving in the first place.

Why a will is not enough - six places where BlockWill works differently

A will is a magnificent legal instrument. It is also approximately five hundred years old in its current form, and it was never designed for a world where 30 to 50% of an HNI’s wealth lives behind passwords.

Here are six places where a BlockWill - used alongside a properly drafted will - does work that a will alone cannot.

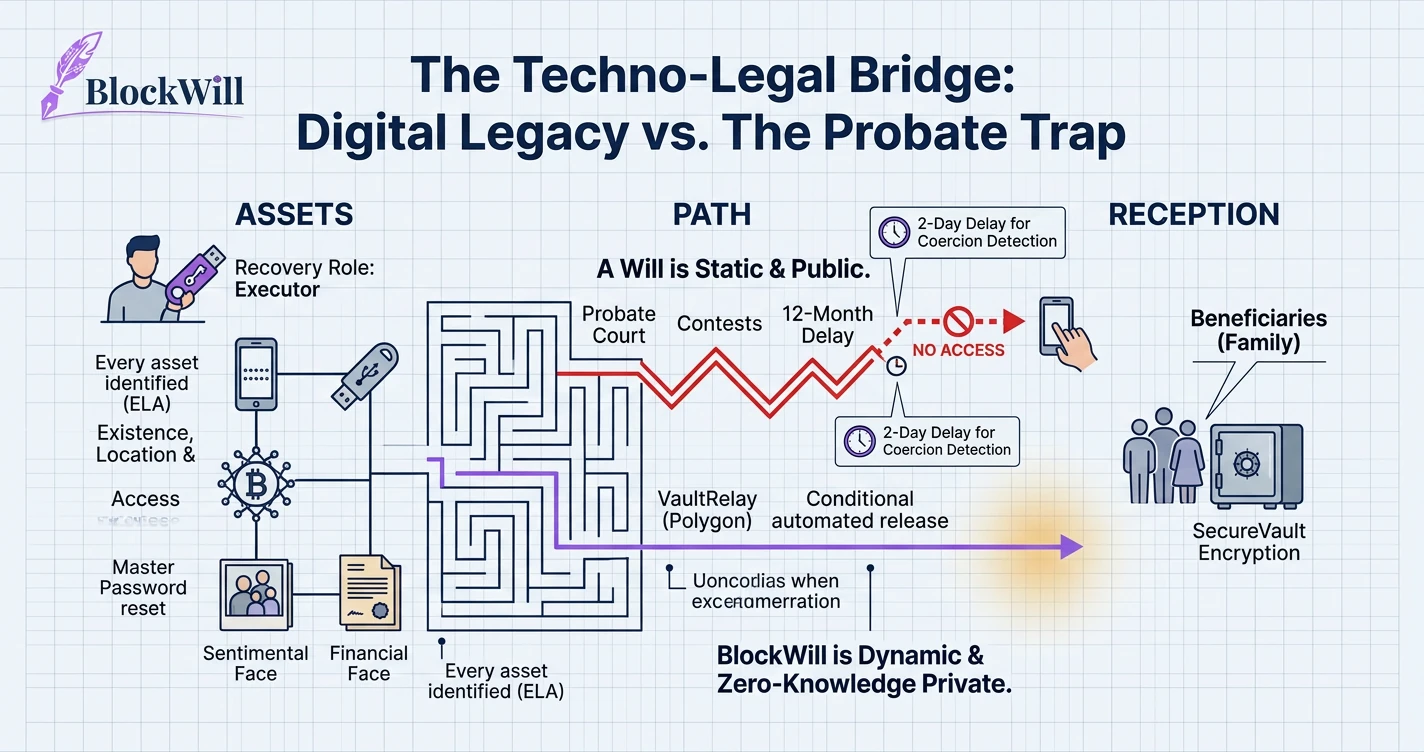

1. A will becomes public during probate. BlockWill is zero-knowledge private.

A grant of probate is a public-record event. Your assets, your beneficiaries, your family relationships, the value of your estate - all of it can become visible to anyone who accesses the record. BlockWill applies zero-knowledge encryption. The platform itself cannot read what is inside the vault. Only the owner and the people the owner explicitly designates ever decrypt it. For HNI families in the GCC, where privacy is itself a form of capital, this distinction matters.

2. A will is silent on existence, location and access. BlockWill provides an ELA roadmap.

A traditional will says “all my remaining assets to my spouse and children equally.” That clause is legally elegant. It is operationally useless if your family does not know what assets exist. BlockWill gives them Existence, Location and Access (ELA) - every asset is identified, every location is mapped, every access protocol is pre-loaded.

3. A will is static. BlockWill is dynamic.

A will written in 2018 does not know about the Binance account you opened in 2021, the ADGM-domiciled fund you invested in last year, or the London property you closed on three months ago. Wealth in 2026 is a moving target - passwords rotate, exchanges migrate, hardware wallets get upgraded. Your estate plan must be a living document, not a notarised photograph of a moment in time.

4. A will depends on probate timelines. BlockWill enables conditional automated release.

Even fast-tracked probate takes weeks. Onshore or contested probate takes 12 to 18 months. BlockWill’s VaultRelay engine releases information conditionally - when the right verifications are present, when the right people are designated, on the timetable the asset owner chose. The court catches up later. The family does not have to wait.

5. A will should not carry login credentials. BlockWill encrypted vaults are built for them.

Every reputable estate lawyer in the world will tell you the same thing - never write passwords or seed phrases into your will. The will becomes a public record, and you have effectively published a theft invitation. So the will stays silent on the very keys that unlock the most valuable layer of a modern HNI’s wealth. BlockWill’s encrypted vault is purpose-built for this layer - seed phrases, two-factor backup codes, hardware-wallet PINs, password manager master passwords, biometric workaround instructions.

6. A will can be contested, lost or forged. BlockWill creates blockchain-anchored evidence of intent.

DigiWish creates an immutable, time-stamped, cryptographically signed record of the testator’s intent at the moment of capture. It does not replace the legal will. It strengthens it. Every recorded intent has a blockchain anchor, which makes it dramatically harder to challenge in court. Several jurisdictions - including Singapore, India and UAE common-law courts - have already accepted blockchain-anchored timestamps as electronic evidence.

What MENA HNIs actually hold - and how a digital legacy fits

A typical MENA HNI’s balance sheet is a mosaic of asset classes, scattered across jurisdictions. Each asset class has its own way of going missing.

- Real estate. Properties in Dubai, Abu Dhabi, Riyadh, London, New York, Mumbai. Sale deeds, title deeds, mortgages, rental agreements live in four different drawers in four different cities. A digital vault holds the documents and the GPS coordinates of where the originals are stored.

- Cash holdings. MENA family offices hold notably more cash than their North American or European counterparts, partly driven by Sharia constraints on interest-bearing instruments. A typical HNI carries three to six banking relationships across Switzerland, London, New York, Singapore and Dubai. Account numbers, RM contacts, signing authorities all need a single source of truth.

- Family business equity. For first and second-generation GCC families, this is still the dominant asset class. Family-owned businesses generate around 60% of UAE GDP. Shareholding registries, shareholder agreements and key-person succession notes are exactly the kind of information that should never depend on the memory of one person.

- Public and private equities. Multi-broker accounts in IBKR, Saxo Bank, Indian demat accounts, US 401(k)s. 28% of MENA family office allocations sit in private equity - cap tables, SPV memberships, drawdown commitments need to be preserved.

- Digital assets. The highest-stakes category. Seed phrases, hardware-wallet PINs, exchange MFA backups. The category most likely to be wiped out by a single moment of forgetfulness.

- Art, watches, classic cars, jewellery, gold. Provenance documents and certificates of authenticity matter as much as the objects themselves.

- Offshore trusts and foundations. DIFC, ADGM, Jersey, Cayman, BVI structures. Trust deeds, foundation charters, trustee contact lists.

- Sharia-compliant investments. About 31% of MENA family offices follow Sharia principles. Sukuk holdings, halal funds and zakat instructions all belong in the inventory.

For each of these, the question is the same - when you are no longer here to tell your family what exists and where to find it, what will tell them?

BlockWill is not a will. It is digital legacy infrastructure.

Let me be precise about this, because it is the most important thing in this entire essay.

A DIFC will, an ADGM will, a Sharia-compliant will, a UK will, an Indian will - these are the products of lawyers, courts and centuries of precedent. They do exactly the work they were designed to do.

What BlockWill does is three things.

It produces electronic evidence - DigiWish - that supports the testator’s intent, anchored to blockchain so that the time, the content and the signature cannot be quietly altered.

It prepares, protects and preserves asset information across encrypted vaults, so that what exists is documented, what is documented is encrypted, and what is encrypted is preserved.

It provides Existence, Location and Access - the ELA framework - to your beneficiaries, on your timetable, on your terms, when (and only when) the time is right.

What BlockWill complements, never replaces, is the work of your private client lawyer, your DIFC or ADGM will, your private bank or family office, and the probate court. We call this the techno-legal bridge - the layer between the certainty of blockchain and the trust of established legal frameworks. It does not compete with either. It connects them.

Armies are for physical safety. BlockWill is for digital safety.

Civilisations have always understood physical safety. We built castle keeps, royal seals, treasury vaults, gold reserves, standing armies. We invest billions in defence ministries because reactive defence - calling for help when the enemy is at the gate - almost always fails. Standing armies exist before the war. Strong walls exist before the siege. This is the most expensive lesson in human history, and we learned it at scale.

We have not yet learned it for digital wealth.

The threats are real and well-known. Lost passwords. Forgotten seed phrases. Master keys held by one person who is no longer here. Cyberattacks. Estate freezes. Probate delays. Family disputes that begin with “but did Dad ever mention …?” Every one of these is a digital-age siege at the gates of family wealth, and most families are still relying on a paper will written before the iPhone existed.

The fall of the Library of Alexandria is the metaphor I keep coming back to. Knowledge that was not intentionally preserved was lost forever. The same is true of a hard drive thrown into a Welsh landfill, an iPhone with a forgotten passcode, or a Binance account whose two-factor backup codes died with their owner.

Here is the thing about a standing army - it is not glamorous. It is mostly invisible until it is needed. It is expensive. It requires discipline. And it is the single most important investment a society makes, because the alternative is unthinkable.

By 2030, one trillion dollars will move across MENA’s families. Twenty-four percent of those families have a real estate plan. The other seventy-six percent are gambling with the most important transfer of their lives. You should not be among them.

If you are a family principal, a family office head, a private banker or a wealth manager in the GCC - let us have the conversation that 73% of your peers are still avoiding. The earlier you have it, the more your family will thank you for it.

That is the work. That is what we built BlockWill to do.